Risk Management Disclosure Report 2025: Executive Summary

The Council of Europe Development Bank (“the CEB” or “the Bank”) Risk Management Disclosure Report provides further information on the Bank’s approach to risk management and the assessment of its capital adequacy. To implement its Strategic Framework, the Bank takes credit, market and liquidity risks to a level compatible with its risk appetite and public mission.

The CEB’s financial strength, as reflected by its Triple-A credit rating, is key to the Bank’s business model as it enables favourable access to the capital markets and low funding costs. Solid key risk measures are essential to sustaining the CEB’s financial strength.

The CEB follows a prudent risk management framework serving the primary purpose of ensuring the Bank’s long-term financial sustainability and operational resilience while enabling it to fulfil its social mandate. Being a multilateral development bank (MDB), the CEB does not fall within the scope of application of the EU legislation on credit institutions. However, the CEB applies international best banking practices that are anchored in the EU directives on banking regulation, the Basel Committee on Banking Supervision recommendations and its status as an MDB.

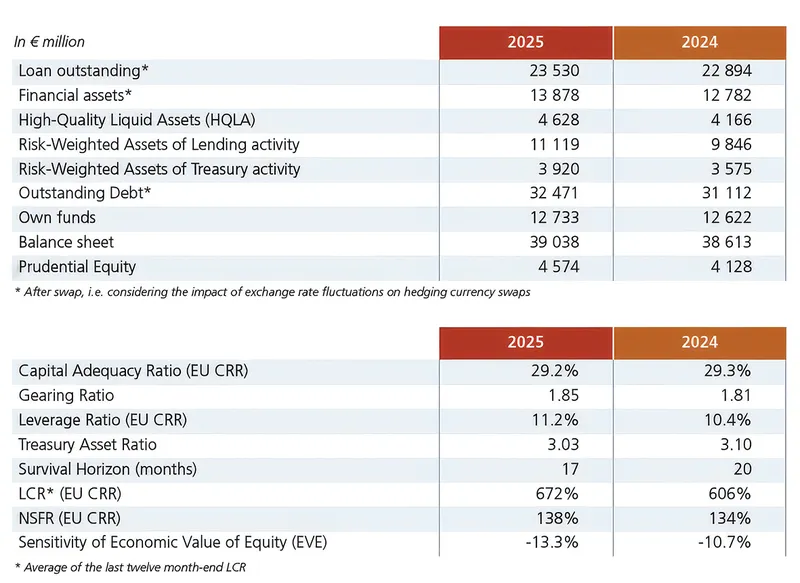

Table 1: Key risk metrics

The CEB has a prudent liquidity management approach, maintaining a strong liquidity position to ensure flexibility in the execution of its funding programme. In terms of market risk, the Bank has no trading activities and uses derivatives only to hedge against interest and foreign exchange risks. The CEB also possesses the required operational resilience as proven by its strong capacity to face challenging financial environments.

In 2025, the CEB increased its lending activity while retaining a sound risk profile and an adequate capital buffer. Loan outstanding reached €23.6 billion (an increase of 2.8% compared to year-end 2024) with new disbursements over the year reaching €3.4 billion.

The credit quality of the CEB’s loan portfolio remains sound, supported by adequate security, guarantees and standard protective contractual clauses. Thus far, no counterparty in the portfolio presents signs of distress and all counterparties are up to date in their payment obligations towards the Bank. Nevertheless, a deterioration in the risk profile could materialise because of geopolitical events or adverse developments in the financial markets, even though current stress test results show that the CEB is in an adequate position to cope with such events. The CEB continues to monitor the situation of its borrowers closely.

Following the CEB’s historic first-ever capital increase with paid-in capital in 2022, the Bank enjoys a strong capital position and the shareholders’ abiding support and confidence in the exclusively social mandate that distinguishes the CEB from other multilateral development banks.

The CEB remains committed to supporting Ukraine in line with the Bank’s Strategic Framework 2023-2027. In 2025, the Bank approved €150 million of new loans to support internally displaced persons (IDP)s, families and households across Ukraine. For an overview of the Bank’s cooperation with Ukraine over the last financial year, please refer to the Annual Report 2025 and to the CEB’s dedicated web pages at coebank.org/en/project-financing/ceb-and-ukraine/our-projects-in-ukraine/.

As a social development bank, the CEB addresses the social impacts of climate change and seeks to achieve climate co-benefits in social projects, notably for the most vulnerable. For more information on climate risk management, please refer to the 2025 Task Force on Climate-Related Financial Disclosure Report.

Despite the challenging financial environment, the CEB’s triple-A credit rating (stable outlook) was reaffirmed by the leading rating agencies Fitch, Moody’s, S&P Global and Scope (unsolicited rating) in 2025. This rating reflects the CEB’s strong capital base, solid asset quality, the excellent track record of asset performance and the solidified institutional profile as a socially focused bank in Europe.

Risk highlights at year-end 2025

⇨ High-quality Assets

- 88.7% of the Bank’s risk portfolio was rated at Investment Grade level (at least BBB-/Baa3 equivalent rating) after Credit Risk Mitigation (CRM):

– 85.3% for the loan portfolio

– 77.5% for the financing commitments

– 100.0% for the Treasury portfolio (deposits, securities and derivatives).

- The average rating of the loan portfolio was 6.98, close to A- (7.0), after CRM (6.99 at year-end 2024).

- 27.1% of the Bank’s loan portfolio benefits from credit enhancement.

⇨ Strong capital adequacy

The Capital Adequacy Ratio (EU CRR1) reached 29.2%, within the 25%-30% comfort zone targeted by CEB to maintain a Triple-A rating by the major credit rating agencies.

⇨ Prudent leverage

The Leverage Ratio (EU CRR) reached 11.2%, well above the regulatory floor of 3%, and the CEB’s Risk Appetite Framework conservative floor of 7%.

⇨ Ample liquidity

The high level of liquidity indicators and ratios protect the Bank from the risks generated by its intrinsic characteristics of absence of collecting deposits and no access to the central bank refinancing.

- EU CRR: European Union - Capital Requirements Regulation and delegated acts.

© CEB July 2026